An estimated one in five Americans aged 65 and older were employed in 2023. This represents nearly a doubling of the share of those who were working 35 years ago. The number of older workers is not only increasing, but their earning power has also grown in recent decades. In 2022, the typical worker aged 65 or older earned $22 per hour. This is a significant increase from $13 per hour in 1987, as reported by the Pew Research Center. 1 On the other hand, many Americans face a significant challenge in achieving financial ability to retire. This challenge is highlighted by an AARP survey, which found that 25% of Americans over the age of 50 who have not yet retired do not expect to be able to retire. Furthermore, one in four individuals in this age group have no retirement savings.2

People Are Working Longer

Financial losses from the Great Recession and the COVID-19 pandemic, as well as increases in the full retirement age for Social Security benefits, are factors that may have reasonably contributed to delayed retirement. The full retirement age has undergone changes over time. For most of Social Security’s history, it was 65. However, this age is gradually increasing. In 2022, the full retirement age was set at 67 for individuals born in 1960 or later. Another factor influencing retirement decisions is longer life expectancy. As people live longer, they will spend more years in retirement, which may require more savings to avoid outliving their money. Typically, accumulating more savings necessitates working for additional years.

However, the decision to work beyond 65 is a personal decision built on answers to some big questions. The answer is personal and depends on several factors, such as your current cash needs, your current health, and family longevity. The answer is personal and depends on several factors, such as your current cash needs, your current health, and family longevity. Some things to consider

Retirement Savings

A 2024 retirement confidence survey found that half of Americans have taken the crucial step to calculate their retirement needs. Following this, 52% of workers and 44% of retirees have increased their savings. Despite 70% of workers and 80% of retirees already saving for retirement, there’s a significant gap between expected and actual savings. Retirement savings should be based on spending needs, not working income. A useful guideline is the 4% safety spending rule, which suggests limiting annual withdrawals to 4% of total savings to last at least 30 years, considering inflation. This rule was designed for classic retirement ages but may vary depending on individual circumstances.

Employer considerations

If you have an employer-sponsored retirement plan or pension, your retirement age may be influenced by your employer’s policies and the financial incentives they offer for retiring at a certain age. This is because employers often have specific rules and guidelines in place for retirement plans, such as vesting schedules and eligibility requirements, which can impact when you can retire and receive benefits. These rules and guidelines are typically designed to balance the employer’s financial obligations with the employee’s needs and goals, and can vary widely depending on the specific plan and employer. As a result, it’s essential to review your plan’s details and understand how they may affect your retirement age and benefits.

Market conditions and economic factors

Economic conditions and the state of financial markets can impact your retirement plans. This is because a strong economy typically offers higher returns on investments, such as stocks and bonds, which can contribute to a larger retirement fund. Retiring during a strong economy may be more advantageous than retiring during a recession. A recession, on the other hand, can result in lower investment returns and decreased economic growth, potentially limiting the funds available for retirement.

Partner perspectives and family considerations

When thinking about retirement, it’s crucial to take into account the viewpoints and requirements of your loved ones, including your spouse, partner, and family. This might entail evaluating the possible advantages of early retirement against the potential downsides, as well as reflecting on the financial impact of supporting adult children or other relatives. Your health and anticipated lifespan are also important considerations. If you are in good health and your parents made it to their late 80s or early 90s, that’s good news. This also implies that if you retire at 62, your savings must cover 25–30 years. But, if you aren’t genetically predisposed to a long life or have a condition that will likely shorten your lifespan, you might choose to access your funds earlier.

Personal goals and lifestyle

When determining an ideal retirement age, several factors come into play. Financial readiness is a key consideration, as working longer can provide additional time to save and pay off debts. Personal fulfillment is also important, as work can be a source of purpose and identity. Continuing to work can provide opportunities for skill development, networking, and access to training and development opportunities. However, working longer can also be physically and mentally demanding, and may limit opportunities for travel and other activities. Ultimately, the decision to work longer should be based on individual circumstances and priorities.

Social Security retirement benefits

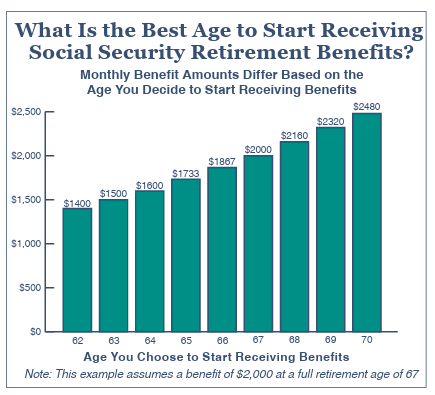

The age at which you can start receiving your full Social Security retirement benefit varies depending on your birth year. You can start receiving reduced benefits as early as age 62, but if you wait until your full retirement age (which ranges from 65 to 67, depending on your birth year), you’ll receive your full benefits. Delaying beyond your full retirement age can yield even larger benefits.

The chart below shows an example of how your monthly benefit amount increases if you delay when you start to receive benefits.

The decision of when to retire will ultimately depend on a variety of factors, such as your individual financial situation, your family’s needs, and your personal goals and aspirations. By carefully considering these factors and weighing the potential benefits and drawbacks of retiring early or delaying your retirement, you can make an informed decision that is right for you and your loved ones. It’s also worth considering the potential impact of your retirement on your family’s dynamics and relationships.

Worried about your financial future? Many Americans share your concern, and there are steps you can take, regardless of how near retirement you are. The trick is to act quickly. The longer you put it off, the harder it can be to change and it is always prudent to consult a financial advisor to discuss your retirement goals, current savings, and potential income sources to determine the best strategy for working longer.

Sources

1. https://www.pewresearch.org/social-trends/2023/12/14/older-workers-are-growing-in-number-and-earning-higher-wages/

2. https://press.aarp.org/2024-4-24-New-AARP-Survey-1-in-5-Americans-Ages-50-Have-No-Retirement-Savings

3. chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.ebri.org/docs/default-source/rcs/2024-rcs/2024-rcs-release-report.pdf