I look forward to writing this market update to share with our clients and our friends what we saw in the market over the past three months and what we see looking forward to the first quarter and the year 2025. I can’t believe another year has come and gone, but 2025, here we come!

Please use the links below to navigate to the sections most helpful to you. This is the shortest my commentary has been in years. I hope you enjoy.

SECTION I – QUARTERLY MARKET REVIEW

SECTION II – MIKE’S COMMENTARY, QUESTIONS, AND QUOTES

SECTION III – TAX CORNER – BENEFICIAL OWNERSHIP INFORMATION FILING

SECTION IV – AROUND THE MWA OFFICE

SECTION V – PICTURES WORTH LOOKING AT

Quarterly Market Review

The 4th quarter of 2024 saw a mixed performance: the US Stock Market grew at 2.63% followed by the Global Bond Market (ex-US) at 0.74%. The other markets fell, with Global Real Estate experiencing the steepest drop at -9.02%, followed by Emerging Market Stocks (-8.01%), International Developed Stocks (-7.43%), and US Bonds (-3.06%). The good news is all these markets, excluding the US bond market (5-year), have shown growth over the past 1, 5, and 10 years. To read the full Market Review Deck. CLICK HERE.

Mike’s Commentary, Questions, and Quotes

My quarterly update, I hope you’ll agree, is better than usual. Howard Marks, founder of Oaktree Capital Management—one of the best investment management firms I’ve encountered and one of the wisest investors of our generation—is well known for producing Memos that highlight the lessons he’s learned during his 50-year investment career.

In a popular You Tube video he said, “Most of the time markets go up and it’s easy to make money, but the challenge is to make money at the same time you control risk, and a portfolio that has the opportunity to make money but with the risk under control, in his opinion, is the mark of a professional investor.” Although some clients may see me as increasingly conservative as I age, I am confident that 7-10% compounded long-term growth can outperform their targets, especially if we can have some dry powder to deploy the next time the markets catch a cold. I know buying when others are spooked will lead to even better returns. A common Millism I say around the office, “the goal is the goal.” We don’t get second chances, we can’t get lost time back, so when we get above the goal and markets are the 2nd most expensive ever, it’s a wise time to play it a little safer than a few years ago when markets were a little less expensive.

History reveals market valuations are driven by investor sentiment, leading to overpricing in euphoric times and underpricing during pessimism. Mr. Marks says, “Managing risk is the most important thing.” We as investors must get this right…and there is no one right. It is what is right for you: your plan, your goals, your expected savings, the time before you need the money, and your need for liquidity. Each of us has a different tolerance for investment pain: the price we must pay to be rewarded with the inevitable gains. Knowing your ability to continue to match forward while your account value is bouncing around is paramount to the way we invest your capital. Remember, even though prices change daily, we still own substantial businesses and important pieces of real estate. These businesses will continue to make profits, and the buildings will continue to produce rents well into the future, especially if we don’t overpay for them.

In the remainder of this letter, here’s what I want you to think about:

- How much am I willing to lose in dollar terms over a 1-year, 5-year, & 10-year timeframe?

- How much decline am a willing to suffer through in percentage terms (from the top to bottom) or (what about over a 3-year period)?

- How much money do I expect to add to my savings over the next 5 years?

My 25-year career in professional money management has taught me that retaining assets during market crashes is more crucial than profiting from booms. Although market euphoria isn’t as pronounced as in late 1999, certain sectors seem overpriced, suggesting potential for price corrections. Today resembles the late 1990s tech boom and bust in many ways, with AI playing a similar disruptive role. Those companies are making AI seem pretty expensive, while many other areas of the markets are just down-right cheap, so Warren Buffet’s teacher Ben Graham’s words still ring true, “Mr. Market makes some cheap every day.” I believe the cheaper areas of the market will continue to produce attractive returns on capital, albeit with some volatility.

Key point to remember when investing: Market Prices for anything are always forward-looking and incorporate every market player’s best guess of the future given what we know today. The future is unpredictable, with some good days and some bad. You can rest assured prices will oscillate between fear and greed as we get glimpses into the future. At some point, the world is going to look really scary (often for some unknown reason). Over the course of a few days or weeks, markets will unexpectedly reprice this new “worry” into prices. When this happens, normally stocks will plummet as liquidity comes out of the system, just like a popped balloon as investors flee for safety (In this dash away from risk, high-quality longer dated bonds usually rise in value which makes them a good hedge to equity).

For stocks like the S&P500, America’s greatest businesses, recovery times vary, but it will probably take 5-10 years to get back the money you had invested in stocks before they fell (not counting new money added or increasing risk after the decline). These fear-based declines are not fun, and they can cause stress and regret. In the past, you have heard me mention the 5-year rule: Any money we need to spend within 5 years needs to be in defensive investments not subjected to the equity market.

Today we can lock in yields of 4.7% for 10 years (Which will return more than this if rates fall). At any time, we can lower risk and accept this rate of return on the portion of the portfolio, not in stocks. My big question for you, do we have enough defense in your portfolio to make you sleep well at night, no matter what happens in the market?

During my writing process- which includes outlining and researching for several days followed by writing daily paragraphs- I came across Mr. Mark’s latest memo on Market Bubbles, which I found so insightful that I chose to link to it rather than extensively quoting it in my work. I hope you’ll take time to read this insightful and wise article while considering my earlier questions. We look forward to discussing these questions with you!

https://www.advisorperspectives.com/commentaries/2025/01/11/on-bubble-watch

All the best,

Mike

Tax Corner – Beneficial Ownership Information Filing

There has been a lot written about the Beneficial Ownership Information (BOI) that was scheduled to be due on January 1st, 2025. That was then changed to January 13th, 2025–and has since been suspended indefinitely. Below is our best effort to show what it is and what to expect in the future.

The (BOI) reporting rules were created to make business ownership more transparent and to stop illegal activities like money laundering and tax fraud. However, these rules have faced legal challenges, which have delayed their enforcement. As of 2025, businesses are not required to report, but they can do so voluntarily.

What is BOI Reporting?

Some businesses must report information about the people who own or control them, called “beneficial owners,” to the Financial Crimes Enforcement Network (FinCEN). A beneficial owner is someone who:

- Has significant control over the company.

- Owns or controls at least 25% of the company.

This system enables law enforcement to track down financial crimes.

What’s Happening Now?

Voluntary Reporting Only: Because of a court decision in Texas (Texas Top Cop Shop, Inc. v. Garland), businesses do not have to file BOI reports with FinCEN right now. If they want to, they can submit reports voluntarily, but there is no penalty for not filing while the court order is in place.

Legal Battles Continue: Some lawsuits argue that the law behind BOI reporting, called the Corporate Transparency Act (CTA), may be unconstitutional. More court decisions will decide if or when the rules will be enforced.

What This Means for Businesses

While the rules aren’t enforced right now, businesses should still get ready by organizing their ownership information and staying updated on any changes.

What Might Be Required in the Future?

If the reporting rules come back, businesses may need to provide details about their beneficial owners, like:

- Full name.

- Date of birth.

- Current home address.

- A document ID, like a passport or driver’s license number.

Penalties for Breaking the Rules

If the rules are enforced again, not following them could result in serious consequences:

- Civil Fines: Up to $500 per day if you don’t comply.

- Criminal Penalties: Up to $10,000 in fines and/or up to two years in jail for intentional violations.

How Can You Prepare?

- Keep up with news about the court cases and rule changes.

- Collect and verify ownership information for your company now, just in case the rules return.

- Talk to a CPA or lawyer to better understand how these rules might affect you.

The Bottom Line

The BOI reporting rules are on hold for now because of legal challenges. Even though you don’t have to report right now, it’s a good idea to prepare. Being proactive can save you trouble in the future if the rules are enforced again. For more details, visit FinCEN’s BOI page.

Around the MWA Office

On her way to be a Certified Financial Planner®

In November, Helen passed the Certified Financial Planner® exam! She is on her way to becoming the 5th member of the firm to hold the CFP®. She will need one more year of experience before she fully becomes a Certified Financial Planner® – but she has done the difficult part.

According to Nerd Wallet,

“A CFP® is a Certified Financial Planner®, an advisor who possesses one of the most rigorous certifications for financial planning knowledge. They must have several years of experience related to financial planning, pass the CFP exam and adhere to a strict ethical standard as set by the CFP Board of Standards.

Unlike some other types of financial advisors, Certified Financial Planners® are held to a fiduciary standard, meaning they are obligated to act in their client’s best interests.

Financial planners who earn a CFP certification must demonstrate proficiency in risk management, investment, tax, retirement, income, and estate planning. This means that they can work with clients to provide comprehensive services across a broad spectrum of financial planning concerns.

CFPs who provide holistic planning can help you to create and maintain a financial plan by determining your financial goals and discussing your current financial situation and appetite for risk. They can also advise on retirement planning, saving for short- and long-term goals, choosing investments and tackling debt.

Some CFPs specialize in a certain area, such as divorce or retirement planning, while others tend to work with specific clients, such as small-business owners or retirees. Because of this, it’s helpful to have an idea of the services you need before you choose a CFP.

There are more than 100,000 CFPs in the U.S. The board reports that 23.8% of CFPs are women, 4.2% of CFPs are Asian or Pacific Islander, 3.2% are Hispanic, and 2% are Black.

The CFP Board is working to serve more people by both recruiting more women and people of color, as well as educating current CFPs on the diverse needs of consumers.

We are so proud of her and the work that she has done with the firm, our clients, and in her studies with the CFP® exam! If you have the chance to speak with her, be sure to congratulate her on this. It is no easy task!

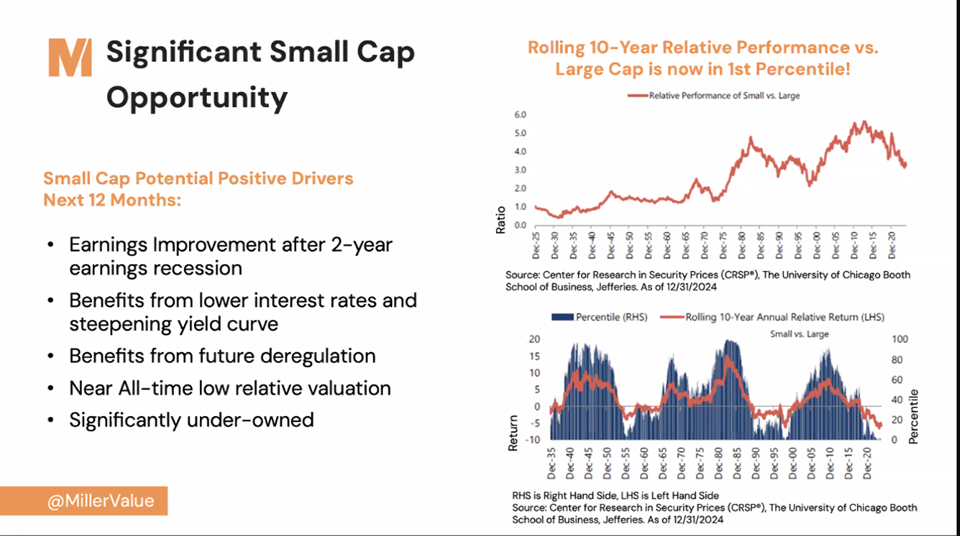

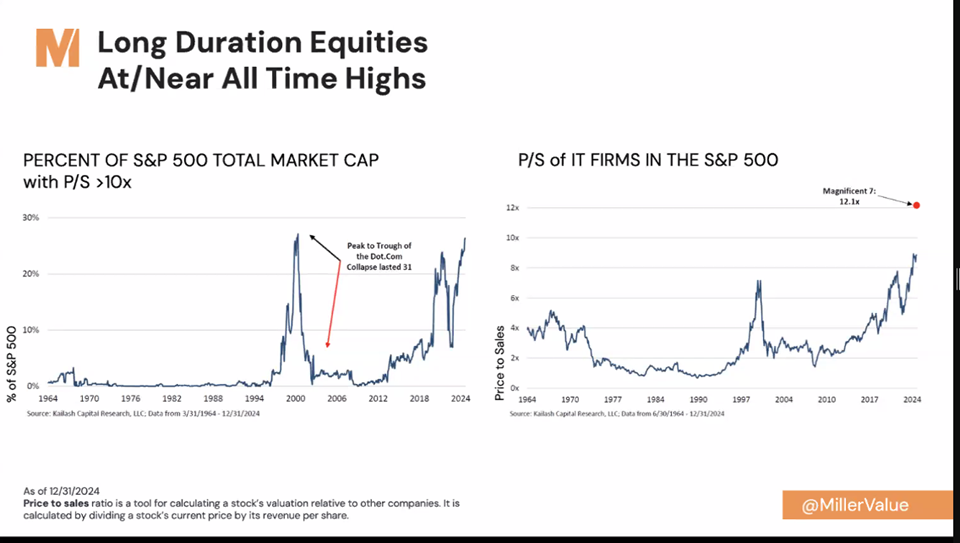

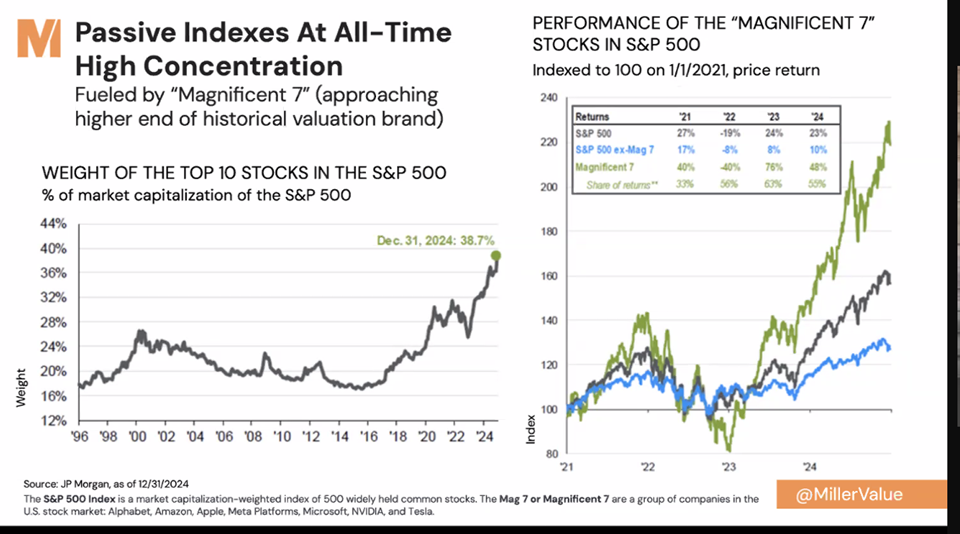

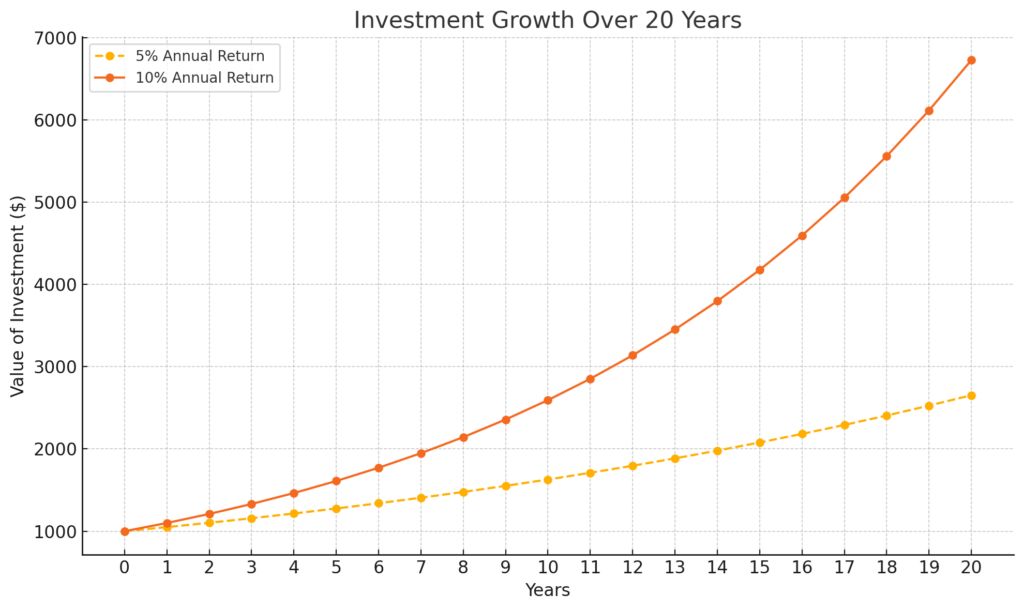

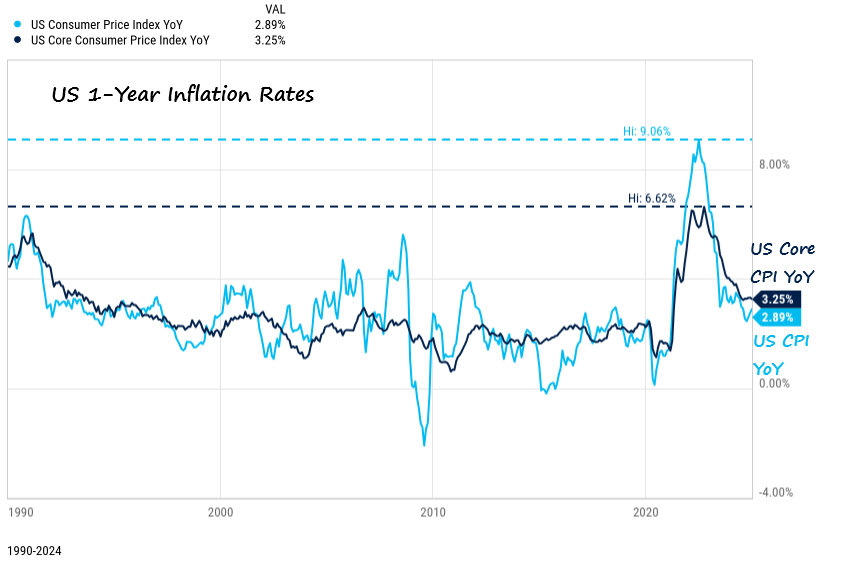

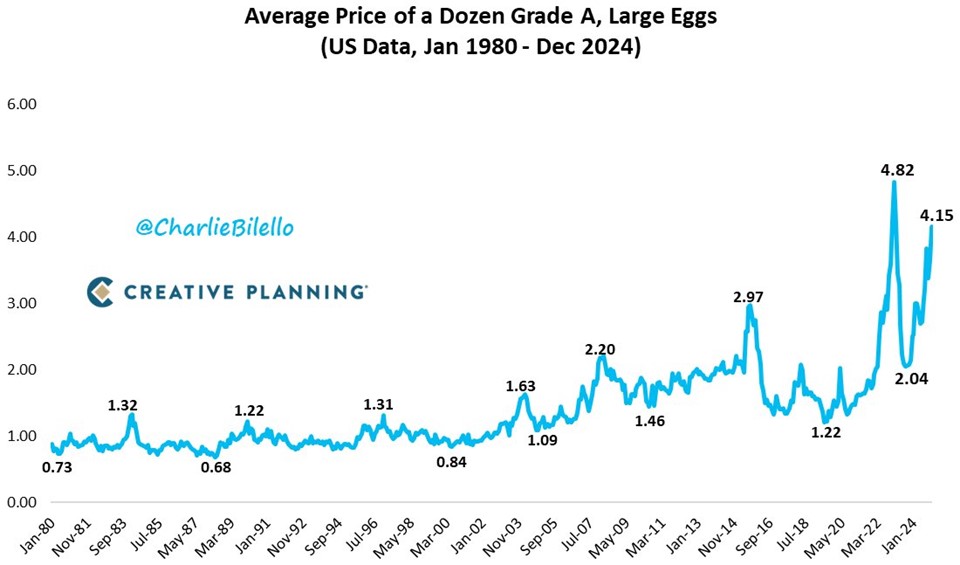

Pictures Worth Looking At