Each quarter, I look forward to writing this market update to share with our clients and our friends what we saw in the market over the past three months and what we see looking forward. It feels like time is in fast forward as the quarter end seems to come faster and faster each year.

Warren Buffett has been known to say, “The stock market is a device to transfer money from the impatient to the patient.” As you know, we think a lot and be patient as we make changes to our portfolios. There are many issues facing investors right now, an election, interest rates, inflation, and a potentially slowing economy to name a few. As your trusted advisors, we are doing all we can to take in information to allow us to give the best advice possible. If you have questions on anything in this newsletter, please reach out so we share any information that may help you feel more confident in your financial situation.

SECTION I – QUARTERLY MARKET REVIEW

SECTION II – MIKE’S COMMENTARY, QUESTIONS, AND QUOTES

SECTION III – TAX CORNER – INHERITED IRAS (POST 2019)

SECTION IV – AROUND THE MWA OFFICE

SECTION V – PICTURES WORTH LOOKING AT

Quarterly Market Review

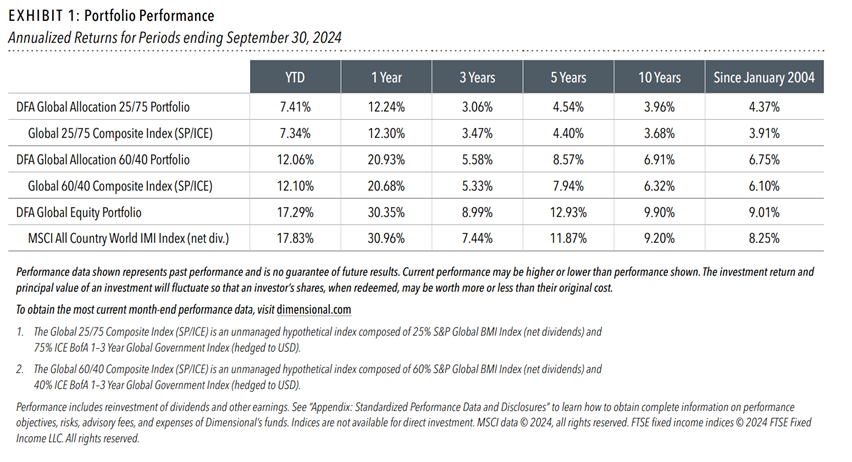

The 3rd quarter of 2024 saw a strong performance with all Stock and Bond Markets across the world were up with Global Real Estate leading the way at 16.04%, followed by Emerging Market Stocks at 8.72%, International Developed Market Stocks at 7.76%, US Stock Market at 6.23%, US Bond Market at 5.20% and finally Global Bond Market ex US at 3.48%. Even better news is that all these markets have been up over the past 1-, 5-, and 10-years. To read the full Market Review Deck. CLICK HERE.

Mike’s Commentary, Questions, and Quotes

1. Reversion to the mean concept (Review your allocation)

2. Why we believe DFA is still the best tool available for equities

Reversion to the Mean: Markets and Market areas will eventually revert to their mean either upwards or downwards…nothing grows to the moon.

- Recent examples- China’s big tech stocks are up 40% in 10 days once they issued stimulus to curb their economic quagmire.

- A couple months ago the Mag 7 went down 10% in a few trading sessions on Japanese carry trade unwind.

- Spread between smallest cheapest stocks and biggest stocks is about the widest it has ever been. Will it revert? Will the spread narrow? (Of course it will, I just don’t know when.)

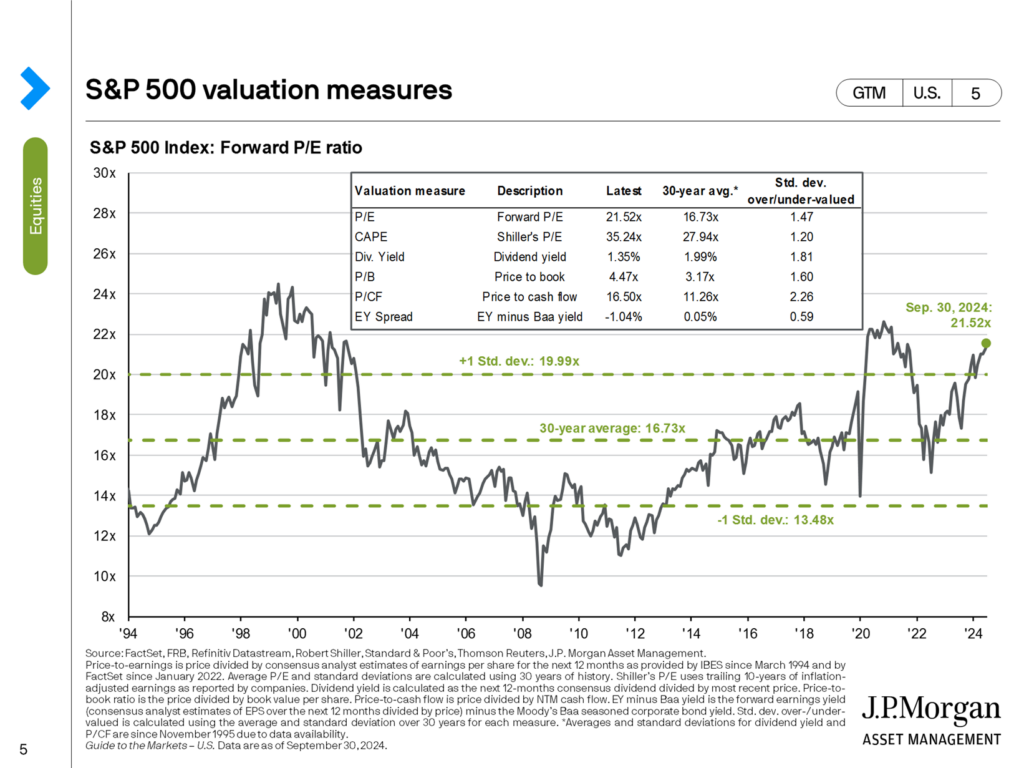

I’ve attached a short article by Weston Wellington titled the Vanishing Value Premium from 2016 that discusses reversion in the value premium in the late 1990s, a period that is probably like today, except with slightly less exuberance. At least, so far. Back then companies did not have earnings, today many of the companies have tremendous profits, but the overall market is probably fully valued, according to GMO we are about 50% above normal mean valuations in the US. (Source: https://www.gmo.com/americas/research-library/a-second-opinion-is-just-what-the-doctor-ordered_9-24_insights/ Buffet is raising cash and sitting on billions more than normal. This is probably as good a reason as any to re-evaluate your allocation, risk, and timeframe. Are you prepared to ride through whatever the future might throw at you with your current allocation?

Client To-do: Re-Review your expected rate of return expectations and the portfolio’s risk characteristics (in dollars and percent change). Making sure you understand the amount your account could fall or decline your portfolio allocation is a great exercise. If any changes need to be made, we would like to do it while we are experiencing large gains not after losses.

In the attached article, the Vanishing Value Premium, Weston Wellington) reviews the last time “Growth” outperformed “Value” stocks in the late 1990s. The Takeaway I want investors to remember: Markets revert their mean returns very quickly. We never know when these changes in prices will occur, only that they will occur, and even though an area of the market may outperform or underperform for a decade, these reversions or changes in price usually happen in a few days or weeks. Will the expensive fall in price, will the underperforming areas rise in price, or will it be some of both? Those changes are hard to predict, but you can rest assured at some point the prices will change, eventually falling or rising to their mean returns. Mean Reversion is the strongest force in finance. It’s kind of like gravity. Investors must be aware that when one area of the market outperforms for a long time (Like many of the biggest Tech companies in America) it gradually sucks investors in, then, when the most are invested, Boom!!! something happens, often unexpectedly and everyone bails, prices over-shoot to the downside, fear is widespread. And just like that, the whole class then trades at or below its mean returns until the buyers return.

This is one of the primary reasons we practice “threshold-based rebalancing” on the accounts we manage. We are constantly counterbalancing paying taxes on unrealized gains compared to your expected future savings that could be used to buy the areas we are underweight with the risk reduction that can come from selling our winners and buying underperforming areas of the markets. As a general rule we don’t like to pay taxes in taxable accounts unless we are way out of whack and don’t have another way to reduce the risk we are unwilling to take.

Rebalance: a technical term we use that describes the process of adding money to areas of the market where portfolios are underweighted or withdrawing funds from positions in the portfolio that have grown and are overweighted.

Why we believe DFA is still the best tool available for equities:

A story about me drinking a little more Kool-Aid. Last week, I spent a few days in Oklahoma with a study group which comprises of a few of my peers that own similarly sized Investment firms from around the old Big 12. As always, it was a great time to share best practices and gather new ideas on how to better serve our clients. Advisors that use Dimensional Funds (DFA) as an investment tool have often been accused of being “cult-like” because of our stubborn conviction in DFA’s evidence-based approach that makes it difficult for other fund providers to earn a spot on our investment roster. Why do outsiders view it as “cult-like”? Besides the fact DFA shares our “client first” mentality, I think it is because they are 1 of a kind. There are tens of thousands of mutual funds, ETFs, and index funds that investors could buy, but they are still one of the few firms I know that only invest based on the belief that predicting markets is too inconsistent and is not worth the time. Instead, they use the information contained in prices to make better implementation decisions and to generate index beating returns by excluding classes of securities with low expected returns and by maintaining greater weighting to securities that pay premiums to market returns.

Think about it this way: If indexes are good, and they have outperformed most investment managers, and they have. DFA has outperforms most equity indexes, so where else can you get an investment that has consistently beaten index returns for 40+ years and that has evolved and continued to win even as markets have changed and evolved?

Dimensional is relentless about finding the best way to systematically capture more of the investment returns available without trying to predict the future (which is unknowable). (Markets are made of up of a lot of smart people and machines, and all of us are usually smarter than just a few of us.)

Let’s look at the numbers in an effort to back up why I am very reluctant to drink someone else’s Kool-Aid:

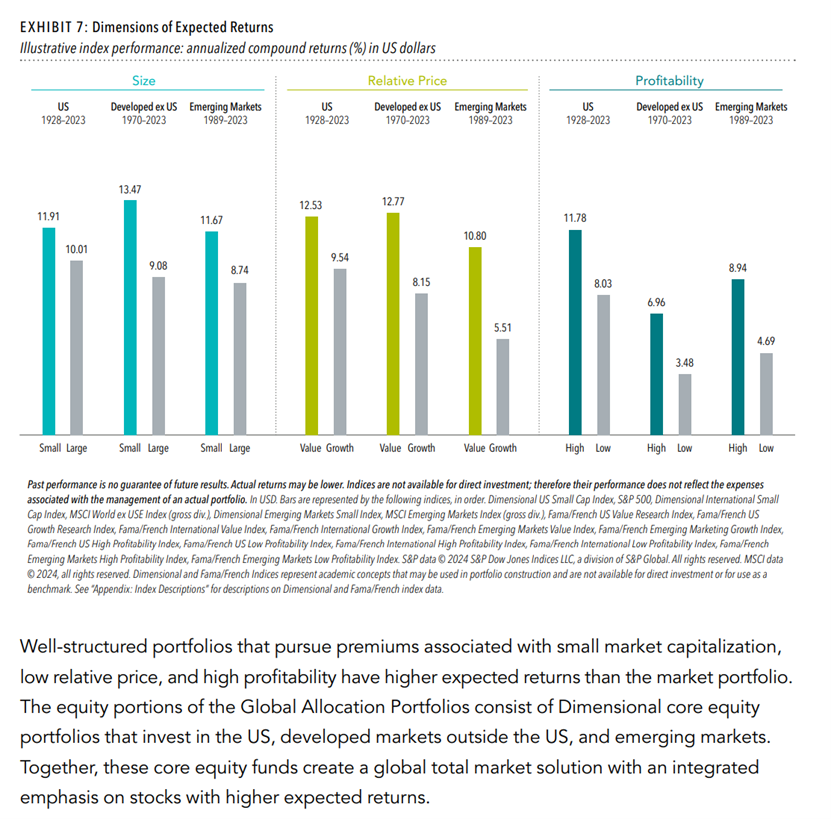

Even in periods of time as short as 10 years (which is pretty short in investment markets) DFA has consistently posted gains in both stocks and bonds) See chart below:

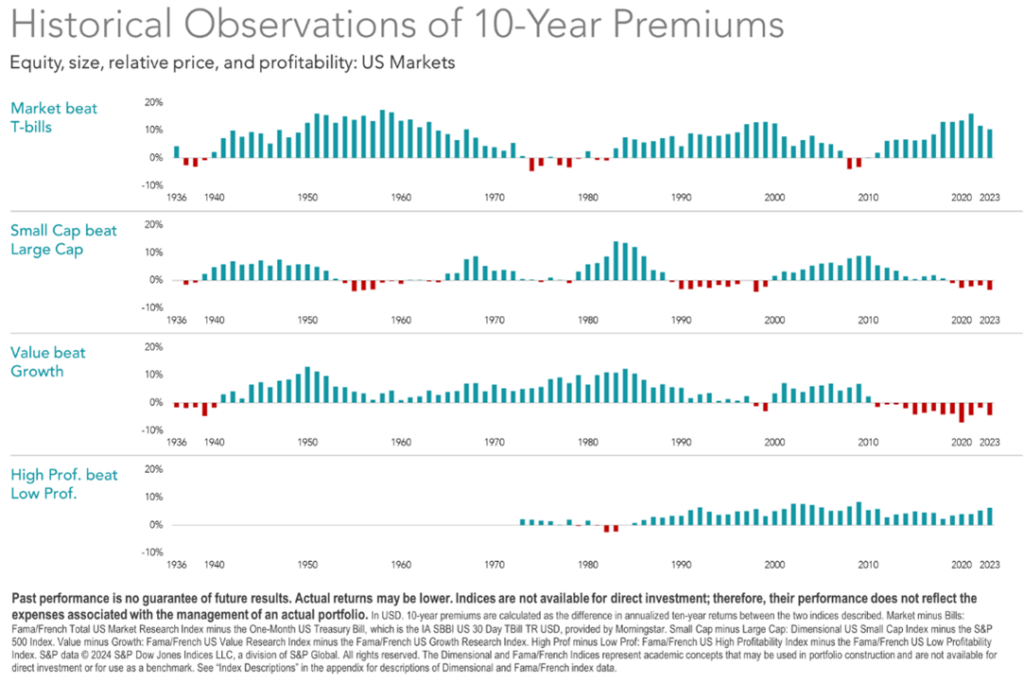

In the picture below this illustrates the 3 Equity Factors (Premiums) DFA fund’s weight towards. I think it is likely that these areas will continue to offer investors premiums in the future similar to their long-term mean returns shown in the picture. Today High profit has outperformed, but Value has lagged. Owning multiple premiums domestically and internationally insures consistent success across time periods.

DFA’s approach and core beliefs are just different than all the other investment companies I’ve uncovered in the 25 years that I’ve been at this. With their 40-years track record of success, just about everything has changed at DFA except their core beliefs that markets are efficient, and that better implementation is the key to winning at the game of investing. They continue to understand their lane and where they do best. They know that portfolio cost have a large effect on investment returns and as they have grown and reached scale, they continue to pass on lower fees to their fund’s shareholders. As a data-driven firm, they measure everything, which can help them prove that the many small steps they take daily managing our money continue to work and create value.

Today DFA offers a full suite of mutual funds, ETFs, and separately managed accounts. This gives advisors like me many different tools to help our client’s reach their goals.

How can I tell DFA is as amazing? One way you can tell is to just look at the 20-30-40 year performance and track record of their funds that have been around that long. This is the easy way. Their record of not closing/merging funds for poor performance is unmatched in the industry. Their track record of outperforming indexes which have outperformed most active managers is consistent and explainable. What DFA managers are doing under-the-hood has changed and evolved as markets have evolved and the tools have changed from mutual funds to Exchange traded Funds (ETFs) to separately managed accounts, but the reasons for their success hasn’t changed.

I could show you this lots of different ways, but I decided to go back and to select DFA’s 1dst product offering their Microcap Fund. It divides the world into 10 slivers largest to smallest and just buys all of the 9’s and 10 smallest companies then excludes the ones likely to go bankrupt and the REITs. Here’s how it has done:

Over 1-1.5% may not seem like a lot,but if you compound that tax efficiently for over 40 years and it is huge.

Currently DFA monetizes 3 Premiums (in equity) that exist in market data. This strategy has been labeled “Factor” investing by the market.

they are still one of the only firms I know that isn’t an index manager and they also only invest based on the belief that predicting markets is too inconsistent and is not worth the time. Instead, they use the information contained in prices to make better implementation decisions and to generate index beating returns.

Think about it this way. If indexes are good and outperform most investment managers and DFA outperforms most equity indexes, where else can you get an investment that has consistently beaten index returns for 40 years through better implementation and that has evolved as markets have changed.

What is required for a Factor to become an investable for DFA?

–Must have a Robust Data Set

–Premium must be Persistent across time periods (it always works)

–Premium must be Pervasive across markets (it can’t be only work in a few places)

On the 1st page of Dimensional Fund Advisor’s website it says “The scientific pursuit of a better way to invest”. “Our daily, systematic approach to outperforming benchmarks and peers sets us apart. We go where the science leads, continually innovating to improve outcomes for investors.” 40+ years of expertise capturing higher returns” How much more proof do you need? If you go look under the hood and you understand how cost, taxes, and turnover from buying and selling effects long-term compounding of money you will understand why I still believe their approach offers investors one of the most reliable and consistent ways to win.

Why is this important to me?

- Because US markets have done well, now is the time decide how much you are willing to lose before the next market downturn arrives. If you want to reduce risk, we want to do it while markets are near highs not after they have lost 20%+. I don’t know when markets will go down, but I am certain that has worked the last 10-15 years is unlikely to be the best performer the next 20 years.

- Decisions do you hold steady where you are currently at?

- Sources of portfolio Defense: Do you feel comfortable about the amount of defense you in bonds or cash/cash value, or hedge fund? If you are still saving money Do you understand the added protection you get from using future savings as defense? If your house is paid off have you set up HELOC. If you are going to count any of this as emergency defense are comfortable with when you would deploy this strategy?

https://my.dimensional.com/dimensional-looks-at-rebalancing-every-day-indexers-cant Explains difference and DFA and Index rebalancing Daily vs 1x per year.

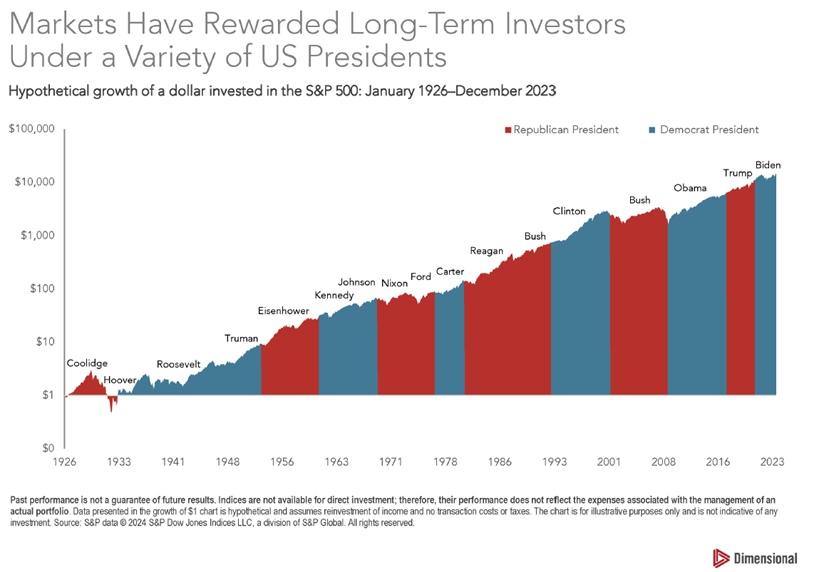

The market and presidential elections: No matter who wins broadly the returns have been almost exactly the same under both parties.

Scouring the market:

You may notice I don’t change the positions in our portfolio very often. It is not because we are not looking. We have a high bar. We are constantly looking for strategies or assets that we think have the potential to make the portfolio have higher returns or that could offer the portfolio less risk in market declines depending on if your portfolio is targeting lower risk, higher returns, or both. Another consideration is taxes. It doesn’t matter what you earn it only matters what we keep. For those investors that are in high income tax brackets we will favor municipal bonds over taxable bonds in most classes. Making this decision results in lower gross returns but higher after-tax yields. The DFA & Vanguard funds we primarily own in our core positions are extremely tax efficient and rarely distribute capital gains, even in years like 2023-2024 where returns were very large. These managers are constantly trying to use every mechanism available to save you money. Dimensional rebalances daily. They use many innovative strategies that may seem like they are picking up pennies, but over 365 days it results in better implementation and shows up in their returns, as they continue to beat their indexes, which are good they just aren’t as good.

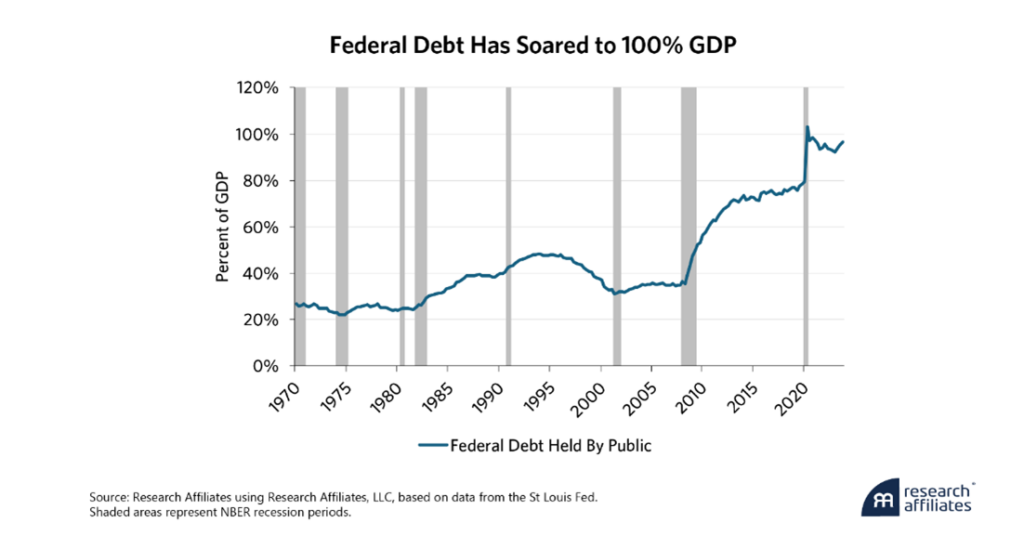

Source: https://www.researchaffiliates.com/publications/articles/1035-stealth-tax-on-prosperity

Immigration and the Economy: This is another interesting article that looks at birth rates and immigration, and how they relate to the United States success. I think we all understand that we must secure the border, but a wise immigration policy is good business.

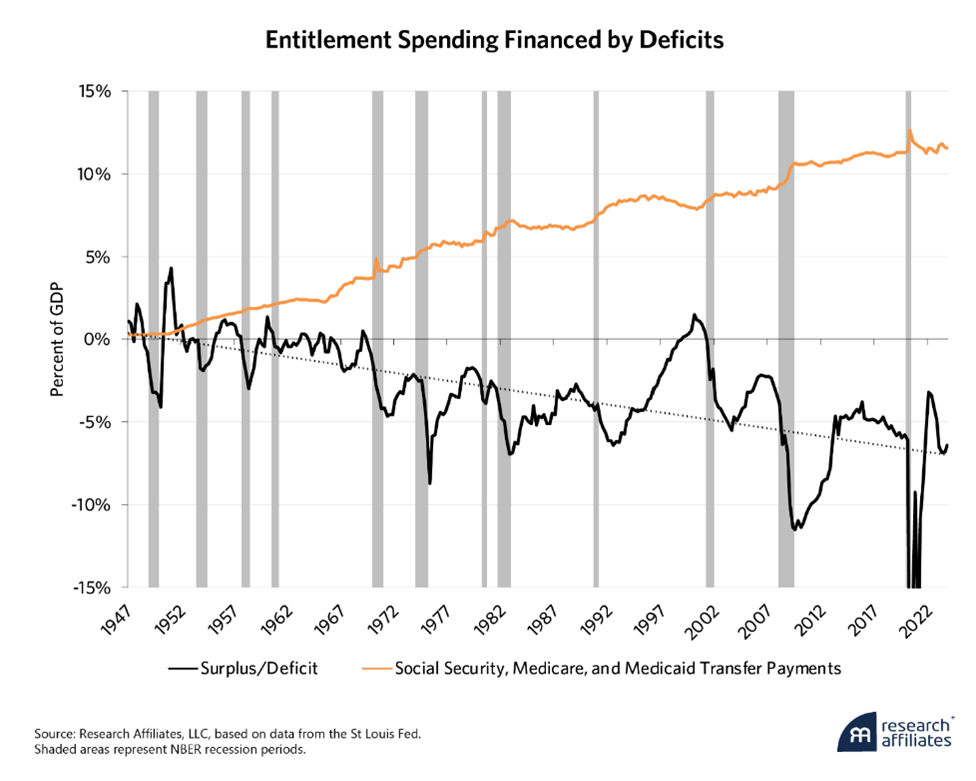

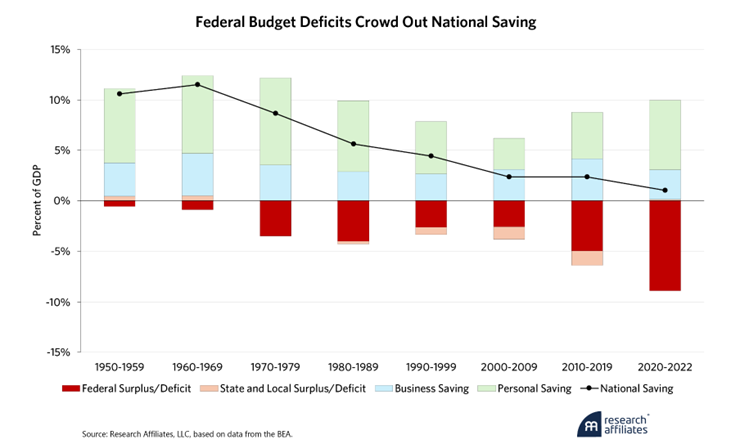

I thought A Stealth Tax on Prosperity was an interesting article. It was packed with good visuals and interesting information that compared spending and saving across decades, but I think my biggest takeaway had to do with paying down our debt and America’s prior budget surpluses. Americans and the Politicians we elect don’t choose to understand that as a country we must eventually address the giant elephant in the room, our ever-growing national debt. Continuing to ignore it puts the dollar as the reserve currency at risk and longer-term it could even impact our discredit our superpower status. We need our government to have the dry powder to freely deficit spend and bridge the economy as we enter large recessions (like the financial crisis or COVID) that cause high unemployment and lower economic activity, however as we come out of these recessions and economic activity resumes and the economy is humming, we must have the fiscal discipline to pay down the debts we accumulated, so we stay fiscally strong and have the capital to get us through the next calamity.

“Recessions thus produce a negative cyclical correlation between public and private saving; government spending of newly borrowed money fills the hole in aggregate demand created by private sector precautionary saving. This process is standard Keynesianism – but only by half. We haven’t followed the other part of Keynes’ policy prescription that requires running budget surpluses to pay down public debt during economic expansions, such as now. This failure is causing the soaring debt and unsustainable deficits discussed above.”

While public and private saving are negatively correlated across the business cycle, they are positively correlated over the long run. The reason is clear. With a publicly provided retirement income, many rationally save less. And when that entitlement spending is financed by public borrowing, negative government saving reduces private saving.

Figure 7:

The second point that I think the article demonstrated is that “Deficits Crowd Out Saving and Depress Investment” which has fueled our technological innovation.

Source: A Stealth Tax on Prosperity By Chris Brightman, Alex Pickard https://www.researchaffiliates.com/publications/articles/1035-stealth-tax-on-prosperity

As always, I hope this newsletter serves as a reminder that we have your best interest in mind. We believe in the Japanese “Kaizen”, which is the pursuit of continuous improvement. We are continuously working to help you reach your goals with the least risk and time. Please reach out and schedule time to talk with us before the year is over so we can make sure you are on track to hit your goals. Invest Wisely, Live Confidently! – Mike

Tax Corner – 2026 Sunset

Now that the Tax Extension deadline has passed, we wanted to remind you to upload your tax return if you haven’t done so yet. To upload a file to our secure system: Click Here.

In 2026, the Trump Era tax changes are set to adjust. This is with both the estate tax and the income tax brackets. In 2026, brackets will adjust back to pre-2017 spots and many of deductions and credits will change. This will include the $10,000 SALT deduction limit, advisory fees and more.

This means that allowing us to have your tax return may be more valuable now than in the past, as it will allow us to help you make decisions in 2024 and 2025 that may no longer be available in 2026, or vice versa. By having your tax return, it allows us to make sure that the investment decisions and/or retirement decisions we help you make will be more beneficial to you. Just about every financial decision you make has a tax impact, so us understanding your taxes is very beneficial to you and us.

Around the MWA Office

In September we hired a new employee. We want to introduce you to and welcome Miguel Rocas to the team! Miguel will be helping Crystal on the client service team and will be helping Mike, Stephen, and Helen on the marketing team!

In other news around the office or “virtual office”, we recently went through a large re-design of our website. We would welcome any and all feedback on the new site. We plan to use it as a place to house informative information for you and your families.

Pictures Worth Looking At