Each Quarterly Newsletter we strive to focus on commenting on the previous quarter. However, after what has transpired the past 10 days in April it feels more pertinent to discuss what is going on right now, mixed in with some of what we saw during the first three months of 2025.

Much has happened in April, and we don’t expect this to be the end of choppy waters in 2025. That being said, we do feel good about where our models are and how we have positioned your portfolio in preparation for the new Trump v China trade war.

SECTION I – QUARTERLY MARKET REVIEW

SECTION II – MIKE’S COMMENTARY, QUESTIONS, AND QUOTES

SECTION III – TAX CORNER – BENEFICIAL OWNERSHIP INFORMATION FILING

SECTION IV – AROUND THE MWA OFFICE

SECTION V – PICTURES WORTH LOOKING AT

Quarterly Market Review

The first quarter of 2025 started off on a positive note, with most major markets posting gains. Leading the way were International Developed Stocks, up 6.20%, followed by Emerging Market Stocks at 2.93%, the U.S. Bond Market at 2.78%, and Global Real Estate at 1.37%. On the downside, the Global Bond Market (ex-U.S.) dipped slightly by -0.17%, and the U.S. Stock Market experienced the largest decline at -4.72%. The good news is that—aside from the 5-Year U.S. Bond Market—all of these markets have shown positive performance over the past 1, 5, and 10 years. To read the full Market Review Deck. CLICK HERE.

Mike’s Commentary, Questions, and Quotes

I will try to keep this shorter than my typical updates because with the market volatility there is plenty of trading to do and conversations to have. I want to apologize for not sending out more daily videos, in the future I think we will start using Twitter(X), LinkedIn, Instagram, and YouTube more frequently to communicate in times of market stress. Hopefully you have seen Stephen’s daily updates on LinkedIn for the past 9 months.

We know sharing and interacting on these platforms will allow us to communicate what we are thinking more frequently and closer to real time.

Let me begin by sharing our trading plan.

Mills Wealth Trading Plan

As you know, we keep some defense in most portfolios to protect against unexpected stock market declines. Having this defense allows us to “buy lower” by typically placing 1-3 trades, hopefully as we approach bottoms, or when things look the scariest. We don’t pretend to know the future, but I think fear is somewhat identifiable by headlines, the VIX soaring over 40, or just be the calls we receive at our office.

Normally money added during a large decline is profitable several years into the future, so we normally attempt to either systematically put money to work overtime, or when fear seems to be at or near the maximum points (like on Wednesday right before President Trump announced the 90-day pause in most Tariffs, except for China.) We were literally entering trades when markets vigorously rebounded, so we decided to wait for another opportunity. I suspect this significant change in global economic policy will not be a V-Shape recovery like COVID.

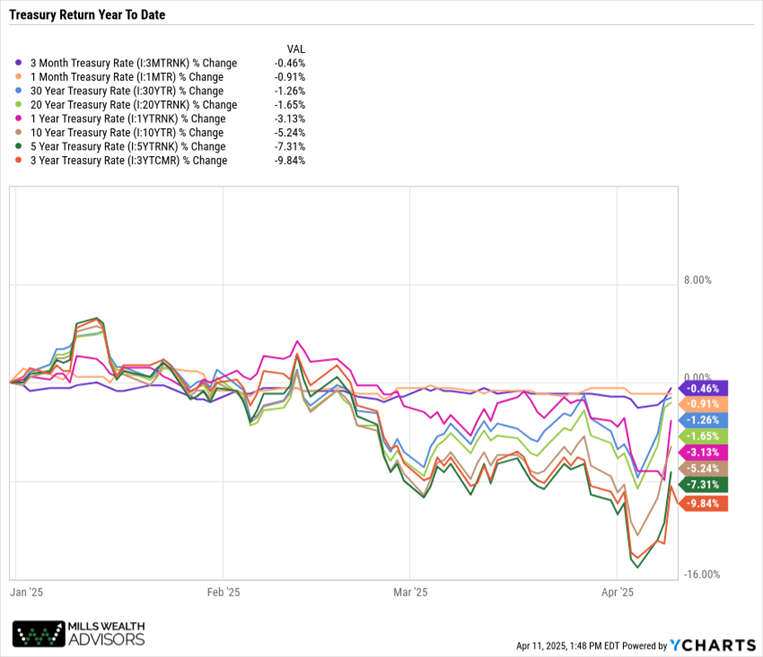

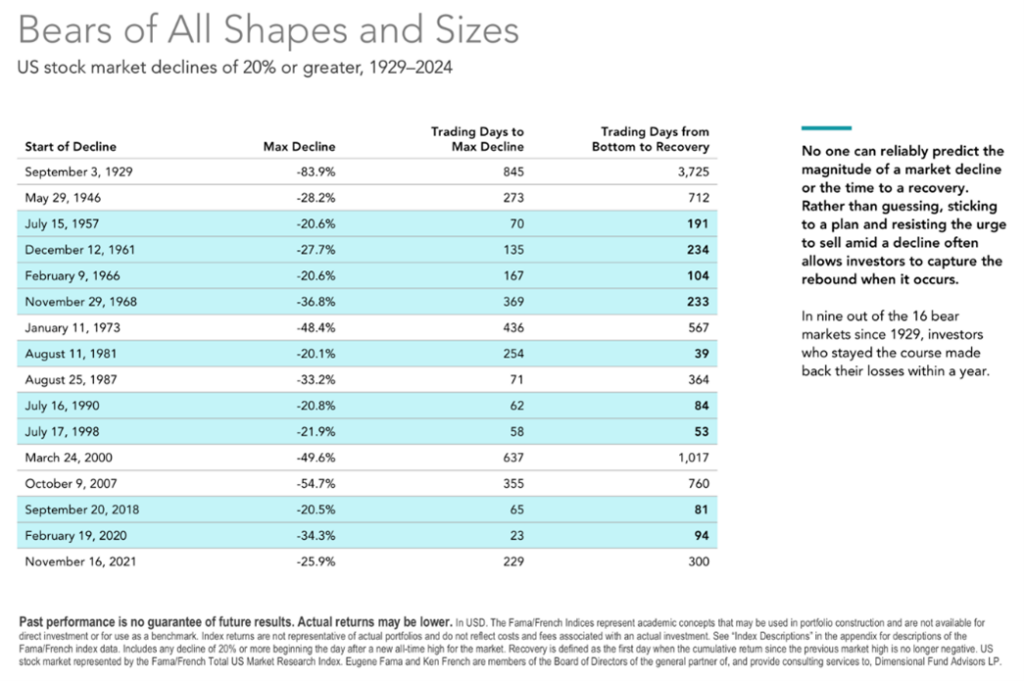

Normally, it takes a while for economic shocks to completely work their way out of market prices. In Figure 1 below, I have included a picture that looks at the magnitude of previous market declines, followed by how many days it took for them to reach the bottom of the market decline, then finally how long it took for the market to fully recover. Notice not all declines rebound quickly. I suspect it is probable that markets will trade in a range as new information unfolds that either lifts markets or causes them to sell off if the news is less favorable than expected. We will use market volatility to attempt to buy on future weakness.

Figure 1

Our current plan is to rebalance 1st, invest any new cash or savings clients send us from accounts outside of MWA or Schwab, bank tax losses for the future in taxable accounts that we can use to offset cap gains on rebalancing trades, and reallocate (meaning we increase the percentage of equities and reduce percentage defense) if markets get cheaper and we see lots of attractively priced stocks. If this happens, we have probably experienced another leg down and we are increasing risk in our models because future market risk tends to be reduced as prices get cheaper (and thus future returns should be larger.) Remember US stocks have had a pretty long winning run and were more expensive than the rest of the world. As is often the case, the cheaper areas of the world declined less than the more expensive areas. Diversification is still our friend.

I suspect markets will trade in a range as the markets digest the proposed tariff impact and the damage inflicted because of the change in US trade policy.

How likely is a recession from what has already occurred?

From what we have researched a 10% tariff and a trade war with China probably causes enough uncertainty to push us into a mild recession at the least. We have seen different estimates of the chance of a recession ranging from 50-75% chance.

Earnings season starts this week and should be strong (estimates call for a 7% gain), fueled by recent surge in buying as the prospect of tariffs caused consumers to speed up purchases of items that are likely to be impacted by tariffs (like cars and I-phones.) It will be interesting to see how company leaders guide future earnings estimates. I suspect future guidance will be more vague or cloudy and eventually we will see Analyst revise company earnings downward which may or may or may not already be reflected in today’s stock prices. Remember markets are forward-looking instruments, today’s prices reflect the fact that most businesses’ future outlooks now have a wider range of possibilities than they had a few weeks ago. That’s why volatility should be higher than normal. We will plan to capitalize on this volatility by adding money to harder hit areas.

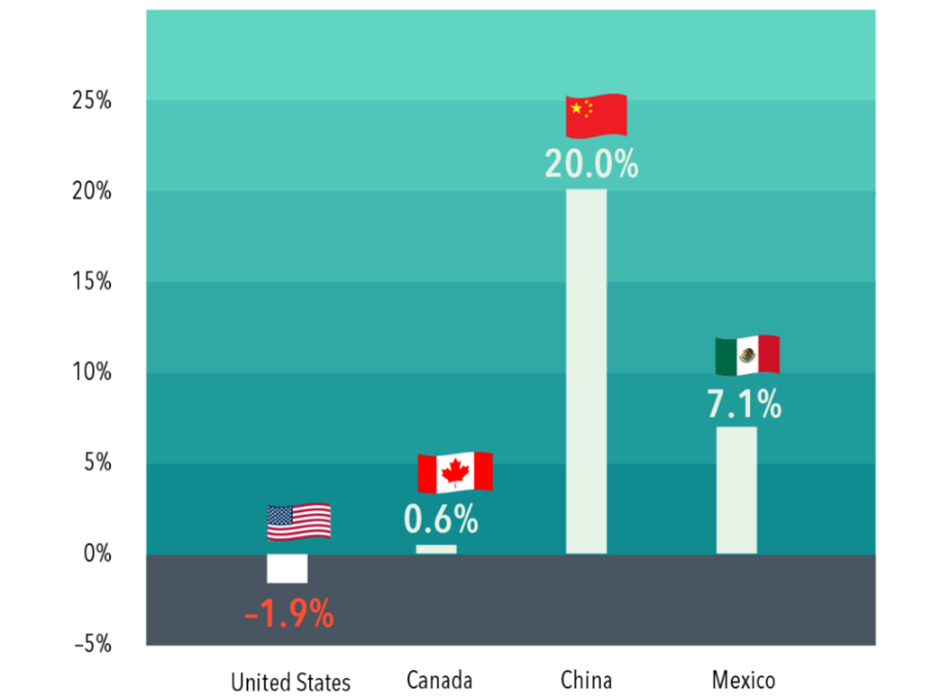

Is this new change in policy good for my investments long-term? It depends. There will be winners and losers. If a company gets its products manufactured in China, this might be a difficult few months as their cost have just increased by over 145% overnight. I doubt much economic activity occurs initially as these companies pivot or wait for a resolution. Both country’s leaders appear to be dead locked in their position and may not be willing to compromise. It is unknowable how this will play out. China has been a poor trading partner stealing our tech, and utilizing other unfair trade practices, so standing up to them and resetting the playing field was needed. I think that diversification will be key to reducing risk.

Global trade is a circular transaction (and supply chains have many interconnected steps. Generally, we send un-backed paper Dollars to China, they send us back finished goods, then they take our dollars and buy our national debt or equity in our businesses in order to keep their currency pegged to ours.

While we are much stronger economically than China, If the trade war escalates from here or just flat breaks our interdependence on each other, I would not be surprised to see China follow through on its threat to take back Taiwan. This could be the kind of event that would send markets falling farther. Should this happen, we would reallocate as described above.

What message do we want you to take away:

Don’t worry, markets are working. While we all hate temporary declines, the real risk is missing out on the permanent ups that will eventually be paid to stocks “rightful owners”. It may be 3-5 years before you realize it, and a few times it has taken a little longer, but it is very likely any money that is added at these levels will produce positive returns. It may take a little while for the money you had invested last week to grow past last week’s highs, but any new savings that gets added or any current defense that gets converted to offense should eventually offer investors attractive returns on their capital.

What can I do to increase my future returns?

Make sure that you are not keeping long-term savings in short-term investments. I’m not referring to emergency funds, but if you have money that is sitting in an account earning interest that is longer-term in nature get it to work into a longer-term investment. Possible Strategy: Pre-invest a year or two worth of your future savings today by lowering your emergency fund and investing it at today’s lower prices (or by slightly increasing your risk) and then saving some of your future savings back into the emergency fund or rebuilding up the defense in the next few years. This helps you deploy more capital while markets are cheaper.

Remember, there is never a good time to panic.

There’s no evidence that companies are less valuable today than they were a week ago, but I think we all know that short-term movements have little to do with logic, it defaults to emotion.

I think we may be entering an unusual time. The tariffs combined with the DOGE reductions in the federal government, the immigration policy changes, and Trumps disregard for the other branches of government will keep uncertainty high, It will be difficult to predict with any degree of confidence how tomorrow’s actions may affect the markets and the economy.

I’ve always found that it is in market downturns like these where some of the best future opportunities get uncovered, so having a little dry powder that you can deploy is prudent.

How do I know the worst is over?

Yesterday at the deepest part of the market decline. I watched Jeffrey Gundlach, an influential bond manager, share his insights on bear markets on CNBC. His best guess was that we were in the Middle innings of this correction. He said, “You don’t stop at average, you gotta get cheap. Somebody’s got to go bankrupt. Bear markets usually end with forced liquidations.” American companies are sitting on billions of debts issued when rates were lower, now rates are much higher requiring much larger payments. As of yesterday (Wednesday April 9th) the longer end of the bond market was rising, indicating foreign investors may have been selling our debt. Trump has said he expects rates to fall, but so far longer rates have gone in the other direction. This is something we will be keeping an eye on.

If longer-term interest rates rise above 5-7%, we will lengthen our bond durations on our defensive assets.

To conclude, every recession is a little different, but we always want to encourage you to look out 5 years from today. While it is possible, we have not seen full scale capitulation, yet markets looked pretty scared yesterday. Re-shoring some manufacturing could realistically take 7-15 years and would have the potential to lead to some inflation from the massive investment that would be required to bring manufacturing back to the US. We will keep our eye on this possibility and will continue to try and insulate our clients from the damaging effects of inflation.

Please don’t hesitate to call or text or email with any questions you might have.

All the Best,

–Mike

Tax Corner – IRS Super Catch-Up Contributions

Starting in 2025, retirement savers in their early 60s will have an exciting new opportunity to boost their savings. Thanks to the Secure Act 2.0, individuals aged 60 to 63 will be eligible for increased catch-up contributions—what’s now being called the “super” catch-up contribution. This change aims to help older workers maximize their retirement funds in their final working years.

Who Qualifies for the Super Catch-Up?

If you participate in a 401(k), 403(b), governmental 457(b), or SIMPLE IRA, and you will be between the ages of 60 and 63 by the end of 2025, you qualify for this enhanced contribution limit. However, once you turn 64, you’ll revert to the standard age 50 catch-up contribution limits. It’s also important to note that not all employer-sponsored plans offer catch-up contributions, so it’s best to check with your plan administrator to see if this option is available to you.

How Much More Can You Contribute?

The super catch-up contributions allow older workers to contribute beyond the usual catch-up limits for a few key retirement plans:

- 401(k), 403(b), and Governmental 457(b) Plans: Participants can contribute the greater of $5,000 or 150% of the age 50 catch-up limit (projected to be $7,500 in 2025). That means the super catch-up limit will be $11,250 for 2025.

- SIMPLE IRAs: The new limit is the greater of $5,000 or 150% of the standard $3,500 age 50 catch-up limit, which means SIMPLE IRA participants can contribute up to $5,250 in additional catch-up contributions.

These increased limits will be adjusted for inflation starting in 2026, so they may increase in future years.

Why This Matters for Retirement Planning

This change is a significant advantage for workers in their early 60s who may have fallen behind on their retirement savings or simply want to bolster their nest egg before retirement. The ability to contribute more in the final working years can provide extra financial security, helping retirees better prepare for their future expenses.

However, with these new contribution tiers, tracking eligibility and limits will become more complex. Employers and plan administrators will need to closely monitor participant ages to ensure the correct contribution limits are applied. Employees, too, will need to stay informed about their eligibility to maximize their savings opportunities before turning 64.

Take Action Now

If you’re approaching age 60 and looking to increase your retirement savings, now is the time to start planning. Make sure to review your current contributions, check with your employer about plan options, and strategize how to take full advantage of this opportunity.

With SECURE 2.0, saving for retirement is getting a boost—make sure you take full advantage of these new opportunities.

Around the MWA Office

ver the past 9 months, Stephen has been posting regularly on LinkedIn and has begun to regularly post on Twitter(X), Instagram and YouTube along with hosting some weibinars. He was the gineau pig for the experiment and you can expect to see more from Mike, Matt, Emily, and Helen in the near future.

We believe that it is important that we share updates, knowledge, and insights often to help you continue to have confidence and clarity in your investments and financial plan.

Consider following/connecting with us on these platforms for more updates and insights.

Mills Wealth Facebook, Mills Wealth Twitter, Mills Wealth Instagram, Mills Wealth YouTube, Mills Wealth Linkedin

Stephen Linkedin, Stephen Facebook, Stephen Instagram, Stephen YouTube, Stephen Twitter

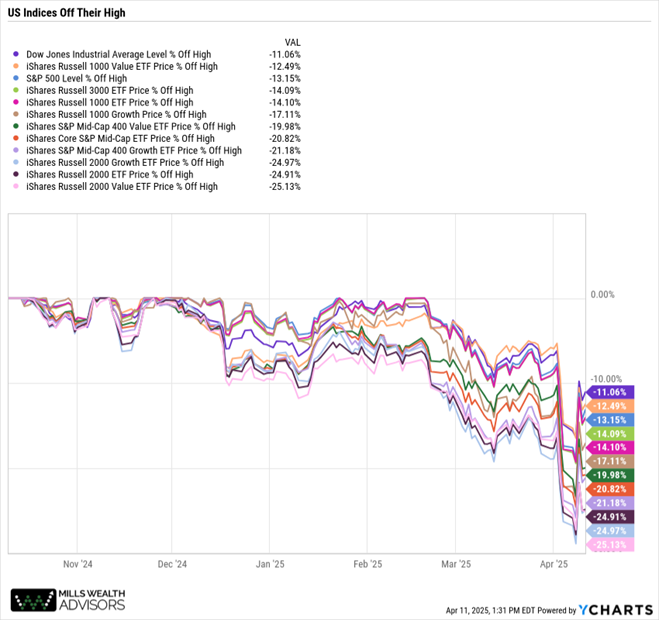

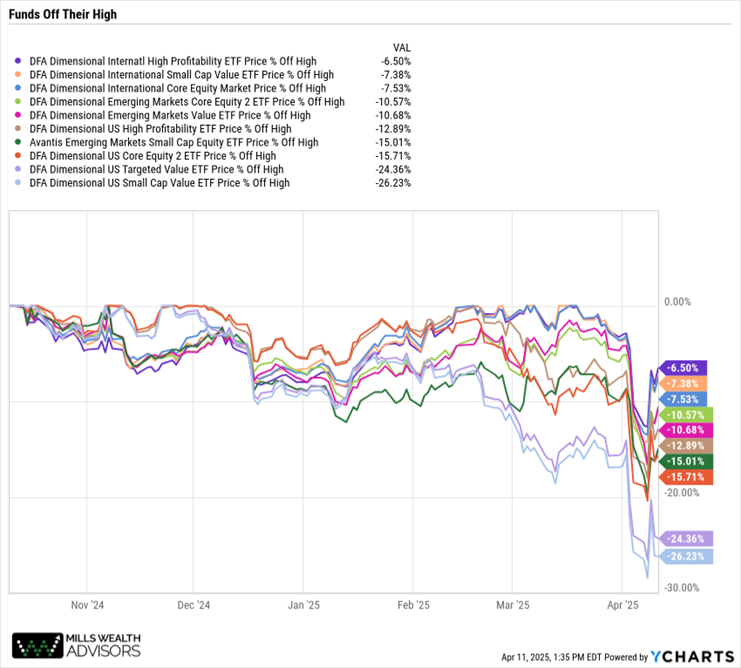

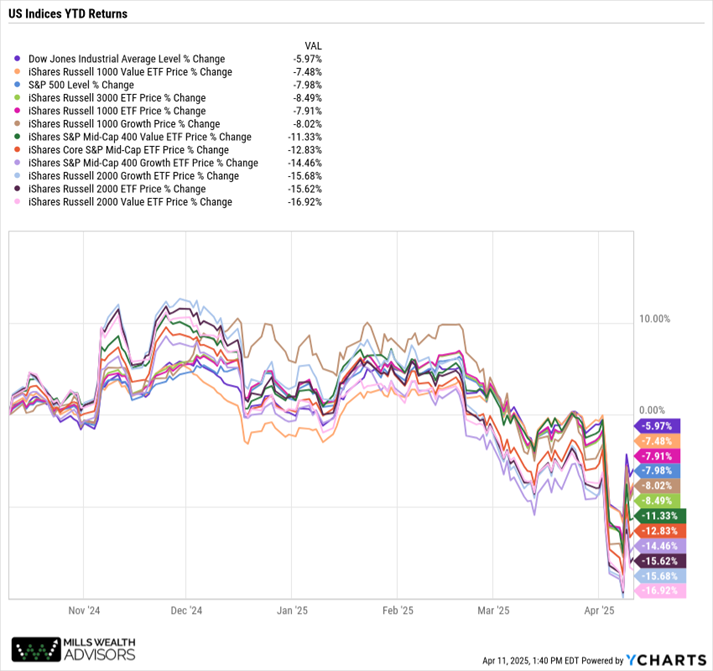

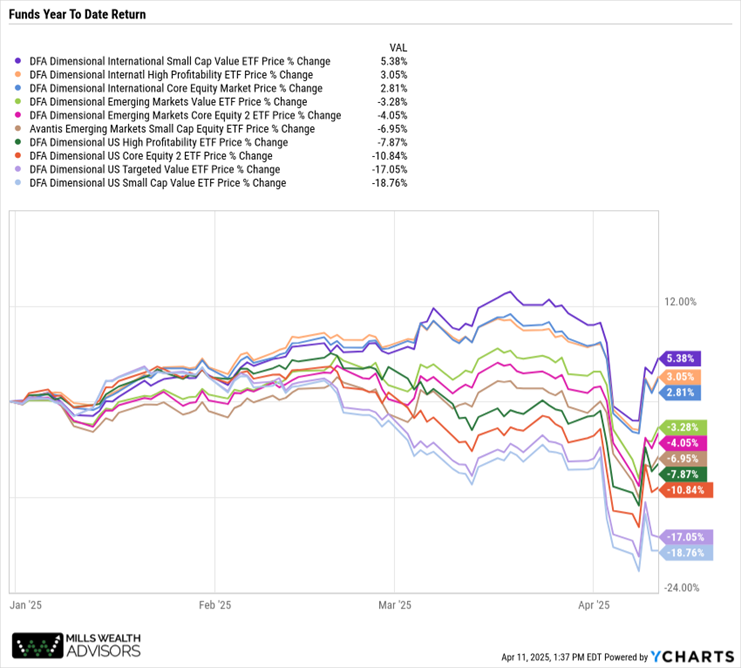

Pictures Worth Looking At